Research on the Comprehensive Competitiveness of Major Global Mining Companies

0. Introduction

The First Industrial Revolution ushered humanity into the steam age, where rapid industrial development propelled mining onto the historical stage and saw the emergence of mining companies. The Second Industrial Revolution marked humanity’s entry into the electrical age, placing higher demands on mining and giving rise to modern mining corporations. The Third Industrial Revolution brought humanity into the technological era, where demand for mineral resources reached unprecedented heights, propelling mining companies into a new phase of high-quality development.Today, with the advent of a new wave of industrial and technological revolution, a new round of technological and industrial transformation—represented by artificial intelligence, new energy, and digital technologies—is reshaping human production and lifestyles. The global mineral resource landscape is accelerating its restructuring, presenting mining companies with unprecedented opportunities and challenges.

Mining companies constitute a vital component of the mining market and serve as its driving force. They shoulder key responsibilities in resource exploration and development, supplying essential raw materials for downstream industrial production and acting as a significant engine for market-oriented economic growth. Among these, major mining corporations stand as core participants in the mining market, commanding substantial market share and playing a pivotal role in guiding and advancing industry development [1–4].Studying the comprehensive competitiveness of major global mining companies is crucial for Chinese mining enterprises to participate in global mineral resource allocation and engage in both competition and cooperation with leading international mining corporations.

Currently, research and analysis on mineral resource strategies and mining markets are extensive and in-depth [5–11], and studies on competitiveness evaluation in the mining sector also exist [12–15]. However, research defining major global mining companies and assessing their comprehensive competitiveness across multiple dimensions—including production, operations, markets, and social responsibility—remains relatively scarce.Therefore, this paper first defines major large-scale mining companies and then scientifically constructs an indicator system for evaluating their comprehensive competitiveness. Using the Analytic Hierarchy Process (AHP), it scores and ranks the 31 identified major large-scale mining companies. The production and operational data of mining companies in this study primarily come from disclosures in capital markets, S&P Global Market Intelligence, and the WIND database.

1. Definition of Major Large-Scale Mining Companies

Currently, no scholar has specifically defined major large-scale mining companies, and there remains considerable confusion across society regarding their classification.For instance, China Shenhua Energy Company Limited (hereinafter referred to as “China Shenhua”), Aluminum Corporation of China Limited (hereinafter referred to as “Chinalco”), ArcelorMittal, and Nutrien are global leaders in coal, primary aluminum, steel, and fertilizer production. However, downstream operations hold significantly greater importance within these companies, with mining production playing a less prominent role compared to other business segments.China Minmetals Corporation (CMGC) is a top-tier enterprise in the industry but is not listed as a whole; Wheaton Precious Metals is an emerging large gold company, but its operations primarily involve purchasing mine output through “metal streams” by paying upfront payments, without actual involvement in mine production;China National Petroleum Corporation (CNPC), Shell, and ExxonMobil are typically classified as oil and gas companies and are not included among traditional major mining corporations;Although Glencore and Luoyang Luanchuan Molybdenum Group Co., Ltd. (hereinafter referred to as “Luoyang Molybdenum”) have significant trading operations, both companies are core mining businesses. Their trading activities primarily support the globalization of their mining operations, thus qualifying them for inclusion in this analysis. Additionally, to ensure access to more reliable and publicly available data, all large mining companies selected for this analysis are publicly listed entities.

Based on the above analysis, this paper defines major mining companies as those whose core business is mine production, which enjoy high recognition within the industry, lead the sector in primary mineral output, demonstrate top-tier operational capabilities, actively fulfill social responsibilities, possess strong comprehensive competitiveness, and have consistently ranked among the world’s top 50 mining companies by market capitalization over the past five years.

Globally, there are approximately 2,000 publicly listed companies involved in mining. After screening, the top-tier major mining companies currently occupying the apex of the industry pyramid total 31 (Table 1), accounting for only about 1.5%.Among these, 16 are diversified mining companies, while 15 specialize in a single primary mineral. Copper serves as the primary mineral for over half of these companies, gold for nearly a quarter, and coal for another quarter.

Table 1 Basic Information of Major Large-Scale Mining Companies

Table 1. Basic Information of Leading Mining Companies

| Serial Number | Mining Company | Primary Mining Operations | Global Industry Standing |

| 1 | BHP Group | Iron ore, copper, nickel, coal | The world’s largest copper producer, third-largest iron ore producer, major coal producer, and major nickel producer |

| 2 | Rio Tinto | Iron ore, bauxite, copper, lithium | The world’s largest bauxite producer, second-largest iron ore producer, third-largest lithium producer, and a major copper producer. |

| 3 | Southern Copper | Copper, molybdenum | Second-largest molybdenum producer and major copper producer |

| 4 | Zijin Mining | Copper, Gold, Zinc | Major copper producers, major gold producers, major lead-zinc producers |

| 5 | Freeport-McMoRan | Copper, Gold, Molybdenum | The world’s largest molybdenum producer, third-largest copper producer, and a major gold producer |

| 6 | Glencore | Copper, cobalt, nickel, lead, zinc, coal, platinum group metals | Second-largest cobalt producer, second-largest nickel producer, major copper producer, major coal producer, major platinum group metals producer, second-largest lead-zinc producer |

| 7 | Saudi Arabian Mining Company (Maaden) | Bauxite, gold | Major bauxite producer, significant gold producer |

| 8 | Newmont Mining | Gold, Copper, Zinc | The world’s largest gold producer, a major producer of lead and zinc, and a significant producer of copper |

| 9 | Agnico Eagle | Gold | Third-largest gold producer |

| 10 | Vale | Iron ore, nickel, copper, bauxite | The world’s largest iron ore producer, a major bauxite producer, a major platinum group metals producer, a major nickel producer, and a significant copper producer. |

| 11 | Anglo American | Copper, platinum group metals, coal, nickel | Major copper producer Major platinum group metals producer Major coal producer Major nickel producer |

| 12 | Fortescue Metals | iron ore | Major iron ore producers |

| 13 | Shaanxi Coal | Coal | Major coal producers |

| 14 | Barrick Gold | Gold, Copper | Second-largest gold producer and significant copper producer |

| 15 | Coal India | Coal | The largest coal producer |

| 16 | Teck Resources | Copper, coal, lead, zinc | Third-largest lead and zinc producer |

| 17 | Vedanta | Lead, zinc, bauxite, iron ore | Major producer of lead and zinc ore, significant producer of bauxite, major producer of iron ore |

| 18 | Antofagasta | Copper | Major copper producers |

| 19 | Luoyang Molybdenum Company (CMOC Group) | Copper, cobalt, molybdenum | The world’s largest cobalt producer, a major copper producer, and a major molybdenum producer |

| 20 | Polyus | Gold | Major gold producers |

| 21 | Norilsk Nickel | Nickel, copper, platinum group metals, cobalt | The world’s largest nickel producer, a major copper producer, a major platinum group metals producer, and a major cobalt producer. |

| 22 | Yanzhou Coal Energy | Coal | Major coal producers |

| 23 | Shandong Gold Mining | Gold | Major gold producers |

| 24 | First Quantum Minerals | Copper | Major copper producers |

| 25 | China Northern Rare Earth | Rare earth | The world’s largest rare earth producer |

| 26 | Salmador Mining and Chemicals (SQM) | Lithium | Second-largest lithium producer |

| 27 | Albemarle Corporation | Lithium | The world’s largest lithium producer |

| 28 | South32 | Coal, bauxite, nickel, lead, zinc | The third-largest bauxite producer, a major lead-zinc producer, a major nickel producer, and a significant coal producer |

| 29 | Jiangxi Copper | Copper | Major copper producer |

| 30 | Anglo American Platinum | Platinum group metals | Second-largest producer of platinum group metals |

| 31 | Tianqi Lithium | Lithium | Major lithium producers |

| Note: Major producers rank among the top ten globally in output of primary minerals, while key producers hold leading positions in global output of primary minerals. | |||

2. Capital Market Recognition of Major Large-Scale Mining Companies

Capital markets serve as a vital engine for driving the development of the mining economy. Given the inherent characteristics of the mining industry—high investment risk, substantial capital requirements, and extended return cycles—it necessitates robust support from capital markets, particularly through public offerings to secure funding.

Capital markets effectively alleviate the financial pressures faced by mining projects due to their long cycles and substantial investments by providing mining companies with diversified financing channels and platforms. Simultaneously, the information disclosure mechanisms and investor oversight mechanisms within capital markets compel mining companies to strengthen internal management and enhance transparency. This is crucial for establishing a company’s solid reputation and attracting more investors.Within an open and transparent market environment, high-quality mining projects gain greater favor from investors and the market, thereby accelerating project advancement and efficient resource development. Furthermore, capital markets facilitate the optimal allocation of mining resources. Through means such as mergers and acquisitions, restructuring, and asset securitization, they assist mining companies in integrating upstream and downstream industrial chains. This enables the realization of economies of scale and synergistic effects, ultimately enhancing the comprehensive competitiveness of enterprises.

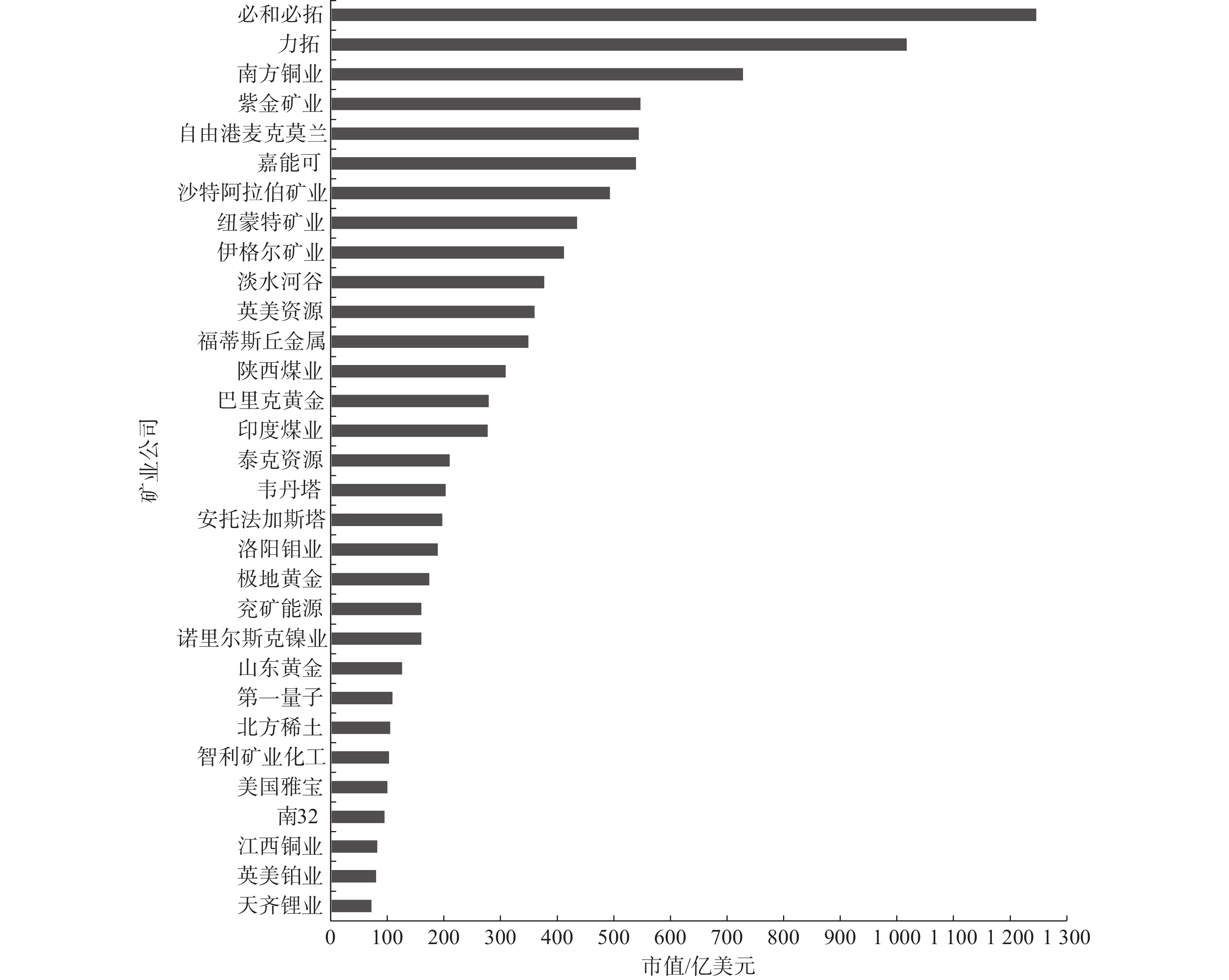

The market capitalization of mining companies serves as the most direct feedback from capital markets, directly reflecting the recognition of these companies by investors and securities market participants.In 2024, the combined market capitalization of 31 major mining companies reached approximately $1 trillion. Among them, two companies exceeded $100 billion in market value, four companies ranged between $50 billion and $100 billion, eleven companies fell between $20 billion and $50 billion, and fourteen companies had market values below $20 billion (Figure 1).

Figure 1 Market Capitalization Rankings of Major Large Mining Companies in 2024

Figure 1. Market value ranking of leading mining companies in 2024

BHP, Rio Tinto, Southern Copper, Zijin Mining, Freeport-McMoRan, and Glencore rank as the top six mining companies by market capitalization, collectively accounting for 46% of the total market value of major large-scale mining firms. All six are diversified mining companies with copper as their primary mineral, while each possesses unique characteristics.Among major mining companies with market capitalizations exceeding $20 billion, four single-mineral-focused firms primarily concentrate on iron ore, gold, and coal. This focus stems from iron ore and coal being bulk commodities with high and stable consumption, while gold, as a precious metal, possesses financial attributes. Among other major mining companies with market capitalizations below $20 billion, a growing number specialize in new energy minerals as their primary focus.

In summary, capital markets increasingly favor diversified mining companies whose core operations center on commodities such as copper, iron ore, and gold. These firms demonstrate strong risk resilience, stable operations, and robust cyclical resistance, with BHP and Rio Tinto serving as the most representative examples.Additionally, in recent years, capital markets have increasingly focused on new energy minerals. Companies like Albemarle (U.S.), Minera Vitacapa (Chile), and Tianqi Lithium have seen market capitalizations surpass those of many traditional diversified mining firms. Diversified players like Rio Tinto and Zijin Mining are also intensifying their investments in new energy mineral assets.

Analysis reveals that mining companies capable of breaking through in capital markets share two key characteristics: first, possessing leading, stable, and sustainable bulk mineral production capacity; second, maintaining stable new energy mineral production capacity and growth potential. However, it is important to note that the market capitalization of new energy mining companies typically exhibits significant volatility and is susceptible to manipulation by speculative factors in capital markets. Over the past five years, their market capitalization fluctuations have exceeded those of traditional diversified mining companies by more than tenfold.

3. Production Status of Major Large-Scale Mining Companies

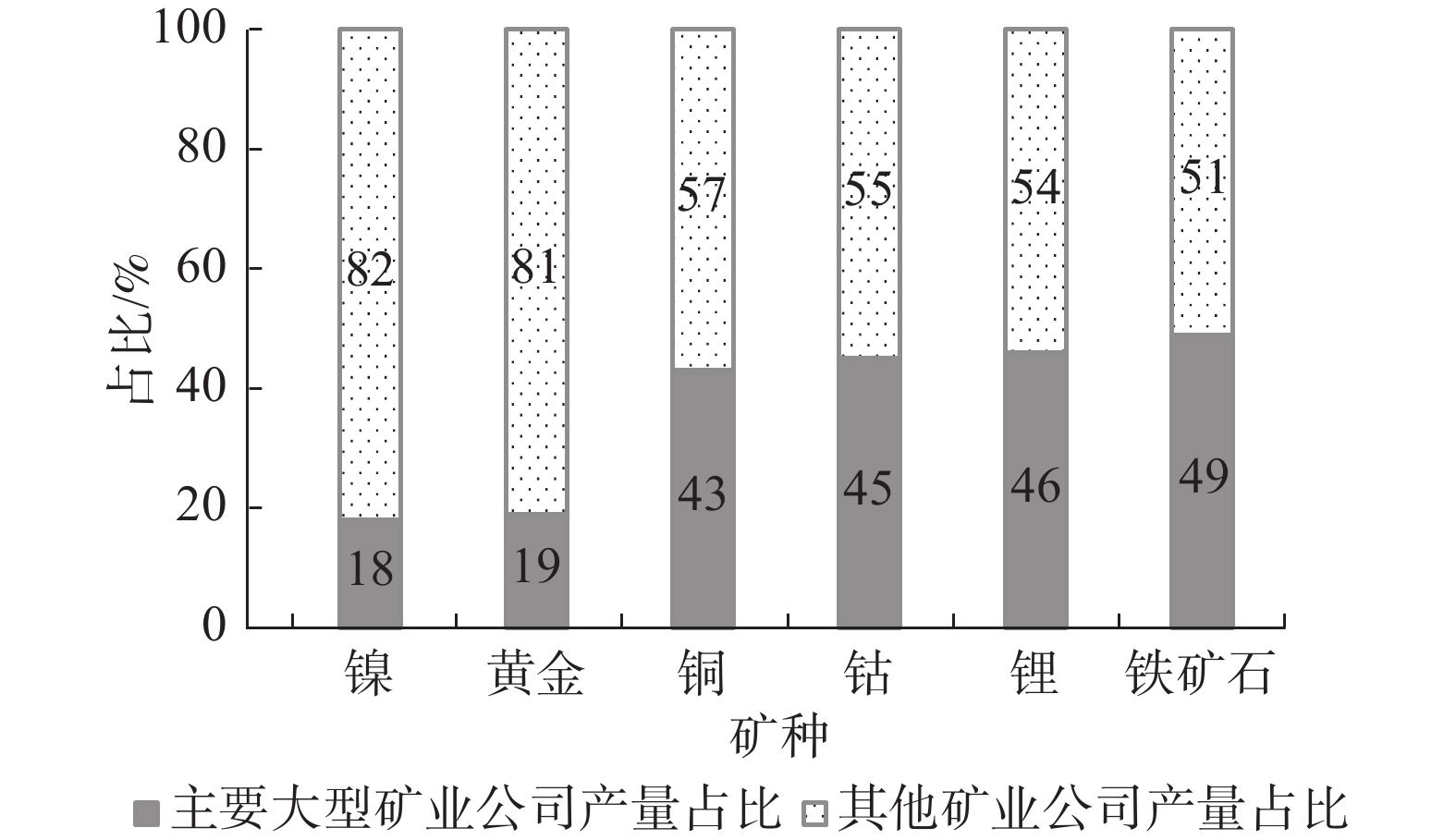

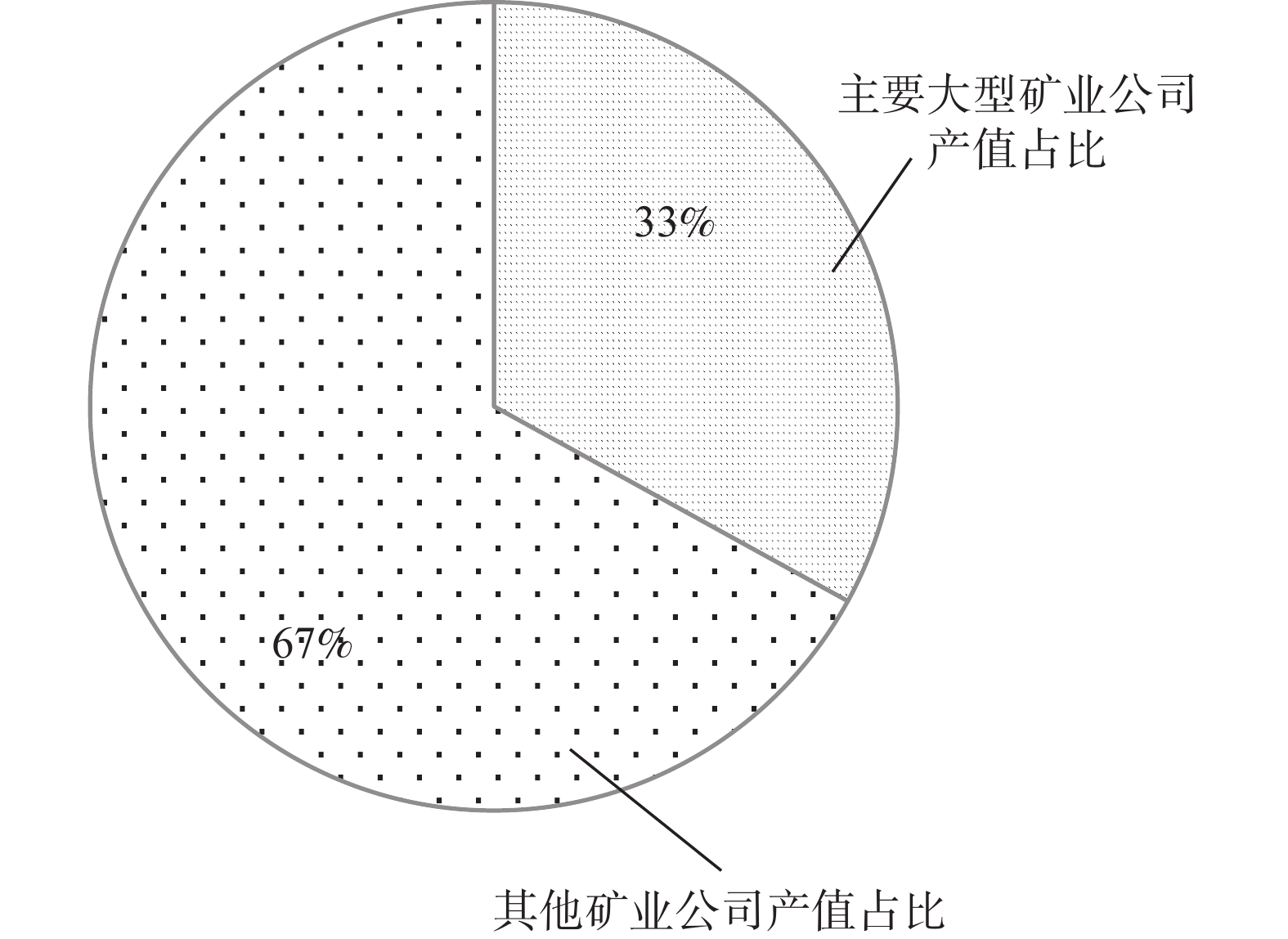

In 2024, 31 major large-scale mining companies produced 49% of the world’s iron ore, 46% of lithium, 45% of cobalt, 43% of copper, 19% of gold, and 18% of nickel (Figure 2). The combined output value of mining projects operated by these 31 major large-scale mining companies accounted for 33% of the global total (Figure 3).

Figure 2 Global Share of Major Mineral Production by Leading Large Mining Companies in 2024

Figure 2. Global proportion of partial mineral production by leading mining companies in 2024

Figure 3 Share of Output Value by Major Large Mining Companies in 2024

Figure 3. Proportion of Output Value of Leading Mining Companies in 2024

Currently, major mining corporations control the majority of high-quality mines globally. Among them, six companies—including Glencore, Newmont Mining, and Rio Tinto—operate over 100 projects each. Fourteen others, such as Barrick Gold, Freeport-McMoRan, and Southern Copper, manage more than 20 mining projects each.Although companies like Tianqi Lithium, Albemarle Corporation, Codelco, and Northern Rare Earth operate fewer mining projects, they control several of the world’s largest and highest-quality mines for their respective mineral types.

These mining companies’ premium mines also host numerous world-class deposits. This article defines world-class mines as those ranking among the top ten globally in annual production for gold, iron ore, copper, bauxite, and coal, as well as those ranking among the top three for other mineral types.Among them, 10 mining companies—including BHP, Rio Tinto, and Glencore—operate more than three world-class mine projects, while 13 companies—such as Teck Resources, Fortescue Metals Group, and Zijin Mining—possess world-class mine projects.

Vale, BHP, Rio Tinto, and Fortescue Metals Group—the four major iron ore giants—control eight of the world’s top ten iron ore projects. BHP, Rio Tinto, Glencore, Anglo American, and Freeport-McMoRan collectively control seven of the world’s top ten copper mines.These mining companies not only develop projects independently but also collaborate on mining ventures. The world’s largest copper mine, Escondida, is jointly operated by BHP and Rio Tinto; the second-largest gold mine, Carlin, is operated by Barrick Gold and Newmont Mining; and the fourth-largest bauxite mine, MRN, is jointly operated by Glencore, N32, and Rio Tinto.

4. Operating Conditions of Major Large-Scale Mining Companies

Major mining companies can be categorized into three tiers based on their total assets in 2024: five companies with assets exceeding $60 billion, seventeen companies with assets between $20 billion and $60 billion, and the remaining nine companies with assets below $20 billion.

Glencore, Rio Tinto, and BHP each hold total assets exceeding $100 billion. With extensive business operations and complete industrial chains, they possess strong resilience against risks. In recent years, China’s mining companies have gradually expanded their scale through mergers and acquisitions. Among them, Zijin Mining’s total assets have continued to climb, currently reaching $58 billion, positioning it to potentially join the top tier.

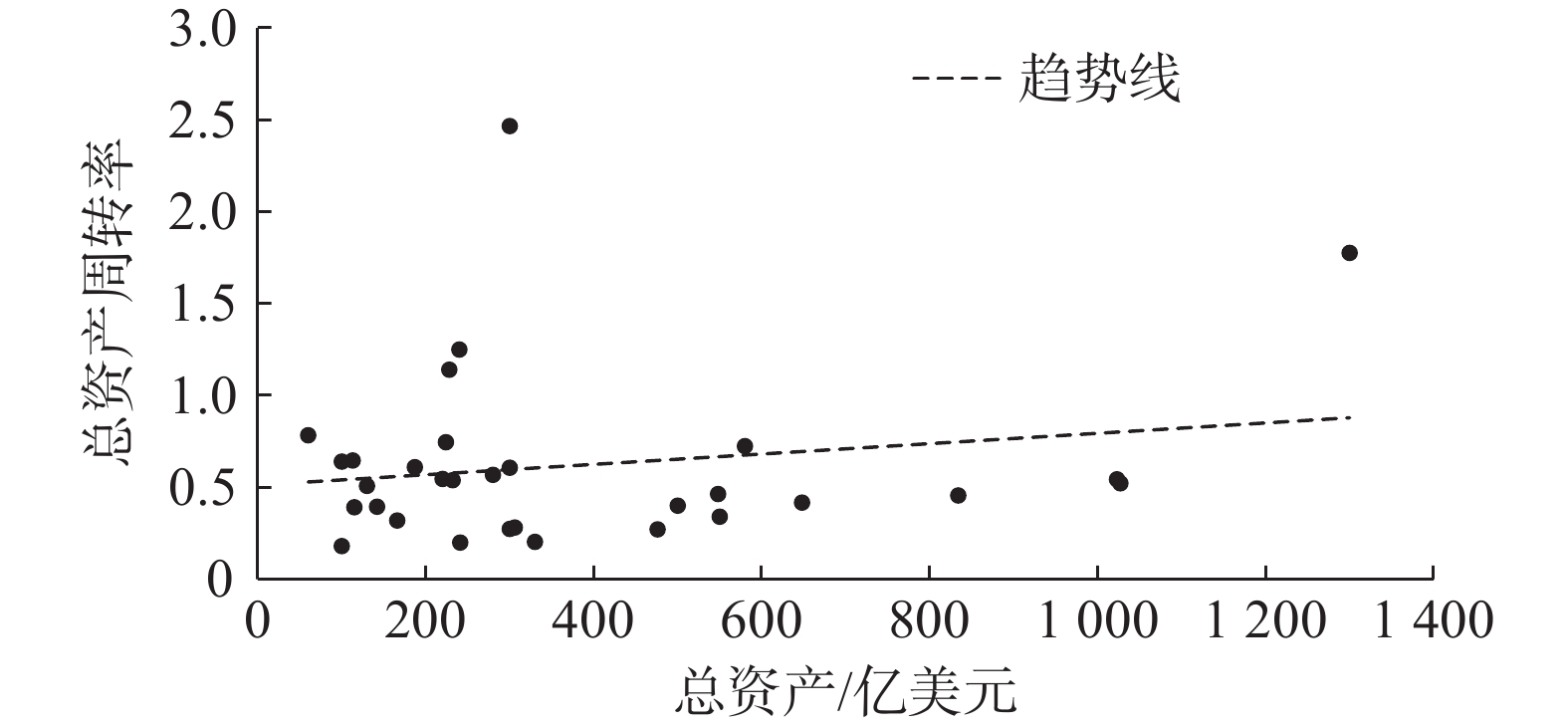

The asset turnover ratio of major mining companies increases with the scale of total assets, indicating that larger mining companies possess a stronger ability to generate revenue per unit of assets (Figure 4). Chinese mining companies demonstrate particularly strong performance in this regard, with half of the top ten companies by revenue-to-assets ratio originating from China.

Figure 4: Relationship Between Total Assets and Asset Turnover Ratio of Major Large Mining Companies in 2024

Figure 4. Relationship between total assets and total asset turnover rate of leading mining companies in 2024

Based on the debt-to-asset ratios of major large mining companies, firms with simpler business models and more streamlined industrial chains tend to have relatively lower debt ratios. Conversely, companies with larger operational scales and more extensive industrial chains generally exhibit higher debt ratios. In recent years, the debt-to-asset ratios of major large mining companies have shown an overall upward trend, with most currently hovering around 50%.

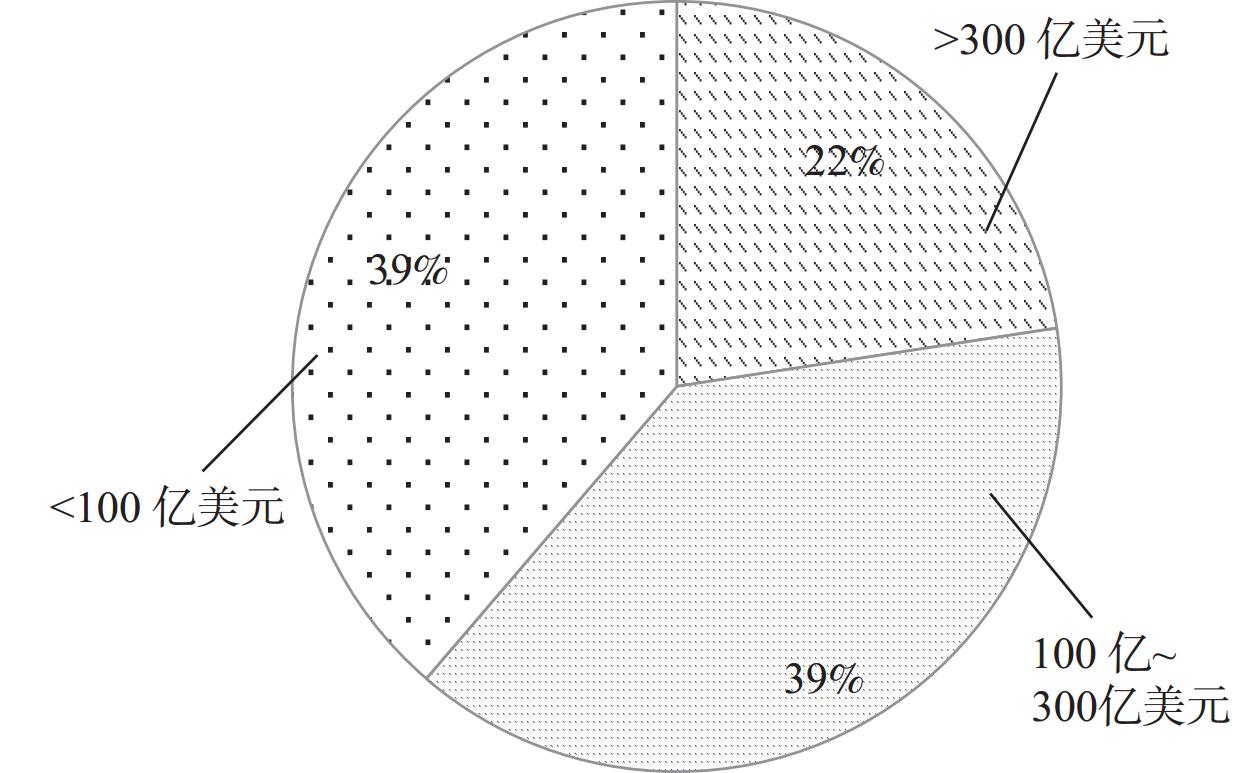

In 2024, seven major mining companies (22%) generated revenues exceeding $30 billion, twelve companies (39%) reported revenues between $10 billion and $30 billion, while the remaining twelve companies (39%) recorded revenues below $10 billion (Figure 5).Among these, the top seven mining companies collectively generated over $520 billion in revenue, accounting for 65% of the total revenue of all 31 major large-scale mining companies. China’s mining companies are strengthening their operational capabilities and global market participation, gradually narrowing the revenue gap with leading Western mining firms in recent years.

Figure 5 Revenue Share by Major Mining Companies in 2024

Figure 5. Revenue Distribution of Leading Mining Companies in 2024

In 2024, six major mining companies (19%) reported net profits exceeding $4 billion, while 11 companies (36%) recorded net profits between $1 billion and $4 billion. The remaining 14 companies (45%) posted net profits below $1 billion (Figure 6).Among these, the top six mining companies collectively generated nearly $40 billion in net profit, accounting for 64% of the total net profit of the 31 major large-scale mining companies.Five mining companies reported net losses, primarily lithium producers whose losses widened due to persistently depressed lithium carbonate prices. Additionally, London Stock Exchange-listed mining giants Glencore and Anglo American also underperformed, though their losses stemmed mainly from multiple asset impairments.

Figure 6 Profit Margin Distribution Among Major Mining Companies in 2024

Figure 6. Profit Levels of Leading Mining Companies in 2024

Western leading mining companies have generally maintained net profit margins around 20% for many years, demonstrating resilience to market fluctuations and sustainable profitability.Chinese mining companies still lag behind their Western counterparts in profitability. While some firms have significantly improved their net profit margins in recent years, their ability to consistently generate stable profits remains to be seen. Overall, mining companies with more diversified primary mineral types tend to exhibit more stable net profit margins. Conversely, those focused on a single primary mineral type are more susceptible to market fluctuations, resulting in greater annual volatility in their net profit margins.

5. ESG Implementation Status of Major Large-Scale Mining Companies

Due to the distinct characteristics of various industries, the environmental, social, and governance challenges they face differ, as do their risk priorities. For mining companies, core concerns primarily include: ecological destruction, water pollution, noise disturbance, dust pollution, greenhouse gas emissions, intrusion into pristine natural areas, labor exploitation, conflict minerals, community conflicts, mine collapses, and harm to miners’ health [17].

ESG stands for Environmental, Social, and Governance, representing an investment philosophy and corporate evaluation standard that focuses on a company’s environmental, social, and governance performance rather than its financial performance. ESG management embodies the concept of sustainable development at the micro level of enterprises, highlighting the impact of environmental, social responsibility, and corporate governance on sustainable business development [18].ESG governance has become a priority for mining development, enabling mining companies to build trust, enhance efficiency, and reduce operational costs[19]. “Environmental (E)” focuses on the ecological impact of mining enterprises during resource development and utilization; “Social (S)” emphasizes relationships between mining companies and their employees, suppliers, customers, and host communities; “Governance (G)” concentrates on management practices, governance structures, and shareholder rights within mining enterprises.

The world’s leading ESG rating agencies include MSCI, S&P Global, FTSE Russell, and Refinitiv. Among these, Refinitiv and S&P Global provide more comprehensive and broader-scope analyses for mining companies. Therefore, this paper primarily re-evaluates and assigns ratings to 31 major large-scale mining companies (Table 2) based on Refinitiv and S&P Global’s ESG ratings, supplemented by each company’s sustainability reports.

Table 2: ESG Ratings of Major Large Mining Companies

Table 2. ESG ratings of leading mining companies

| Level | Company |

| A | BHP, Rio Tinto, Zijin Mining, Vale, Freeport-McMoRan, Newmont Mining, Luoyang Molybdenum, Norilsk Nickel, Codelco, Tianqi Lithium |

| B | Glencore, Southern Copper, Fortescue Metals Group, Eagle Mining, Coal India, Vedanta, Jiangxi Copper, Shaanxi Coal Industry, Teck Resources, Saudi Arabian Mining, Shandong Gold, Yankuang Energy, N32, First Quantum, Antofagasta, Northern Rare Earth, Albemarle, Anglo American Platinum |

| C | Anglo American, Barrick Gold, Polar Gold |

Grade A indicates the company possesses strong management capabilities and sustainable development capacity, with extremely low ESG risks; Grade B indicates the company possesses relatively strong management capabilities and sustainable development capacity, with relatively low ESG risks; Grade C indicates the company possesses average management capabilities and sustainable development capacity, with certain ESG risks.

The ESG performance of mining companies has become a core concern for investors, regulators, and the public, directly impacting their financing capabilities, operational standards, and overall competitiveness. It has thus emerged as a critical strategic element for the survival and development of mining companies.

6. Comprehensive Competitiveness Evaluation of Major Large-Scale Mining Companies

The Analytic Hierarchy Process (AHP) was first proposed by American scientist Tal Ben-Shahar in the 1970s. This method categorizes all elements involved in decision-making into three primary levels: objectives, decisions, and alternatives. It represents a research approach that integrates qualitative and quantitative analysis [20]. By reducing the subjectivity of human judgment, AHP serves as a scientific methodology for decision research.

Numerous factors influence the comprehensive competitiveness of mining companies. After analysis, this paper categorizes them into three primary factors: market, resources, and finance; and seven secondary factors: market capitalization, number of mining projects, number of world-class mines, revenue, net profit, total assets, and environmental, social, and governance (ESG) performance. Using the Analytic Hierarchy Process (AHP) and based on research into these seven secondary indicators, this paper provides a comprehensive competitiveness evaluation of major global mining companies.

The application of the Analytic Hierarchy Process (AHP) in evaluating the comprehensive competitiveness of major large-scale mining companies can be divided into the following four fundamental steps: First, establish a clear hierarchical model for assessing the comprehensive competitiveness of major large-scale mining companies; Second, construct a discrimination matrix based on expert scoring and discussion results, using the numbers 1 to 9 and their reciprocals as discrimination scales to define the discrimination matrix for the comprehensive competitiveness of major large-scale mining companies (Table 3), with the specific expression shown in Equation (1);Third, calculate the weight vector Wi using the arithmetic mean method, and compute the one-time indicators CI and CR (RI selection values are shown in Table 4). The specific expressions are given in Equations (2) to (4). When CR < 0.1, the consistency of the discrimination matrix for the comprehensive competitiveness of major large mining companies is considered to have passed the test; otherwise, the discrimination matrix needs to be reconstructed.Fourth, the hierarchical overall ranking and consistency of the comprehensive competitiveness of major large mining companies are tested. To more scientifically evaluate investment regions, this study employs a method combining expert comparative scoring with big data analysis, assigning different weights to each indicator based on the Analytic Hierarchy Process (AHP) (Table 5). Finally, the comprehensive competitiveness ranking results for major large mining companies are obtained (Table 6).

Table 3 Meaning of Discrimination Matrix Scales

Table 3. Meaning of discriminant matrix scale

| Scale | Meaning |

| 1 | Indicates that the two factors are equally important when compared. |

| 3 | Indicates that, when comparing two factors, the former is slightly more important than the latter. |

| 5 | Indicates that, when comparing two factors, the former is more significant than the latter. |

| 7 | Indicates that the former factor is significantly more important than the latter. |

| 9 | Indicates that, when comparing two factors, the former is far more important than the latter. |

| 2, 4, 6, 8 | Median value between two adjacent judgments |

| Countdown | If the ratio of the importance of factor i to factor j is a_(ij), then the ratio of the importance of factor j to factor i is a_j = 1/a_(ij). |

Table 4 Standard Values for Random Index (RI)

Table 4. Mean Random Consistency Index RI Standard Value

| Matrix order | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| RI | 0 | 0 | 0.58 | 0.90 | 1.12 | 1.24 | 1.32 | 1.41 | 1.45 | 1.49 |

Table 5 Indicator Weights

Table 5. Indicator Weight

| Objective | Primary factors | Secondary factors | Weight |

| Comprehensive Competitiveness of Major Large Mining Companies | Market | W1 (Market Capitalization) | 0.278 |

| W2 (ESG) | 0.049 | ||

| Resources | W3 (Number of Mines/Projects) | 0.177 | |

| W4 (Number of World-Class Mines) | 0.085 | ||

| Finance | W5 (Revenue Tier) | 0.213 | |

| W6 (Net Profit Level) | 0.070 | ||

| W7 (Total Assets Level) | 0.128 | ||

| λmax (maximum eigenvector) | 7.420 | ||

| CI | 0.070 | ||

| CR | 0.053 | ||

Table 6 Scores of Major Large Mining Companies

Table 6. Score of Leading Mining Companies

| Serial Number | Mining Company | Score (after percentage conversion) | Corporate Level |

| 1 | BHP | 100 | mining giant |

| 2 | Rio Tinto | 100 | |

| 3 | Glencore | 94 | Top Mining Companies |

| 4 | Zijin Mining | 93 | |

| 5 | Vale | 91 | |

| 6 | Freeport-McMoRan | 81 | |

| 7 | Newmont Mining | 77 | Leading large-scale mining company |

| 8 | Southern Copper | 72 | |

| 9 | Fortiscu Metal | 69 | |

| 10 | Anglo-American Resources | 67 | |

| 11 | Eagle Mining | 66 | |

| 12 | Indian Coal Industry | 66 | |

| 13 | Barrick Gold | 65 | |

| 14 | Luoyang Molybdenum Co., Ltd. | 63 | |

| 15 | Norilsk Nickel | 62 | |

| 16 | Vedanta | 61 | |

| 17 | Jiangxi Copper | 61 | |

| 18 | Shaanxi Coal Industry | 61 | |

| 19 | Tec Resources | 58 | Major mining companies |

| 20 | Saudi Arabia Mining | 55 | |

| 21 | Shandong Gold | 52 | |

| 22 | Yankuang Energy | 48 | |

| 23 | South 32 | 47 | |

| 24 | First Quantum | 45 | |

| 25 | Antofagasta | 41 | |

| 26 | Chilean Mining and Chemical Industry | 40 | |

| 27 | Tianqi Lithium | 40 | |

| 28 | Polar Gold | 39 | |

| 29 | Northern Rare Earth | 38 | |

| 30 | Albarel, USA | 38 | |

| 31 | Anglo American Platinum | 35 |

BHP and Rio Tinto are the world’s only two mining giants, possessing top-tier resource production capabilities and financial strength. They demonstrate a strong commitment to corporate social responsibility while enjoying high recognition in capital markets, enabling them to stand out in any mining cycle.Glencore, Zijin Mining, Vale, and Freeport-McMoRan have joined the ranks of top-tier mining companies. Firms at this level demonstrate formidable industry competitiveness across resources, finance, and markets, possessing a degree of risk resilience, though they still lag significantly behind the mining giants.Twelve companies—Newmont Mining, Southern Copper, Fortescue Metals, Anglo American, and others—are classified as first-tier large mining companies. These firms possess strong industry competitiveness, with some capable of ascending to the top tier during favorable market conditions, though their risk resilience remains moderate.Thirteen mining companies, including Teck Resources, Saudi Arabian Mining, Shandong Gold, and Yankuang Energy, are classified as general large-scale mining companies. These companies possess a certain level of industry competitiveness but are significantly affected by mining market cyclical fluctuations. They have the potential to join the ranks of first-tier large-scale mining companies but also face the risk of falling out of the main category of large-scale mining companies.It should be noted that the Analytic Hierarchy Process (AHP) inherently involves subjective judgment. Furthermore, due to incomplete disclosure of data on reserves, production, and technology by some mining companies, the indicators selected in this paper exhibit limitations in terms of systematicness and comprehensiveness. Consequently, the results represent only a comprehensive competitiveness ranking based on the aforementioned indicators chosen for this study.

7. Conclusions and Recommendations

1) Globally, there are approximately 2,000 listed mining companies. Among them, the 31 major mining corporations occupying the top tier of the industry pyramid account for only about 1.5% of the total. Yet these companies produce 33% of the world’s mineral resources by value.

2) Capital markets increasingly favor diversified mining companies with core operations in minerals such as copper, iron ore, and gold, as well as new energy mining companies. However, new energy mining companies are more susceptible to speculative manipulation in capital markets, resulting in significantly greater market capitalization volatility compared to traditional diversified mining companies.

3) Among major mining companies, those with larger asset scales and more diversified primary mineral types tend to exhibit greater operational stability. Conversely, companies specializing in a single primary mineral type are more susceptible to market fluctuations, resulting in greater annual volatility in financial metrics such as revenue and net profit.

4) The ESG performance of mining companies has become a core concern for investors, regulators, and the public, directly impacting their financing capabilities, operational standards, and overall competitiveness. Major mining corporations regard it as a critical strategic element for their survival and development.

5) Comprehensive research analysis indicates that BHP and Rio Tinto are currently the only two global mining giants; Glencore, Zijin Mining, Vale, and Freeport-McMoRan rank among the top mining companies;Newmont Mining, Southern Copper, Fortescue Metals, Anglo American, Eagle Mining, Coal India, Barrick Gold, Luoyang Molybdenum, Norilsk Nickel, Vedanta, Jiangxi Copper, and Shaanxi Coal have entered the ranks of first-tier large mining companies;Teck Resources, Saudi Arabian Mining, Shandong Gold, Yankuang Energy, N32, First Quantum, Antofagasta, Minera y Química de Chile, Tianqi Lithium, Polar Gold, Northern Rare Earth, Albemarle, and Anglo American Platinum were classified as general large-scale mining companies.

6) The new wave of industrial and technological revolution is accelerating the reshaping of the global mineral resource landscape. China’s mining companies face unprecedented opportunities and challenges. It is recommended that major large-scale mining companies in China currently adopt a steady and pragmatic approach, enhance their operational capabilities, create greater value for the nation, society, and shareholders, and exercise caution in pursuing mergers and acquisitions. Priority should be given to strategic alliances between strong companies to address operational and management weaknesses.

This document is a reprinted article.